An ECN broker links you to an electronic trading network where banks, non-bank dealers, brokers, and sometimes other traders all stream buy and sell prices and trade with each other.

Instead of your order going to a single dealing desk, it enters a shared pool of bids and offers from many participants. The prices you see come from that network of quotes, not from numbers created inside a retail broker’s dealing room.

On the screen, an ECN account still looks like any other trading platform. You pick a symbol, see a bid and ask, and send orders. The difference sits underneath. Fills should come from a central book, spreads should move with real interbank conditions, and the broker should earn mainly from commission and small mark-ups rather than from systematically taking the other side of your positions.

For traders who already know the basics, the ECN label triggers a few questions. How close are spreads to interbank. How much of my flow is really going into a shared book. Is the broker actually neutral on my profit and loss, or just using the label as marketing.

Answering those needs a clear view of how an ECN works, how brokers hook into it, and how that setup compares with the more familiar market maker and STP models that dominate retail trading.

How an ECN actually works

ECN matching engines

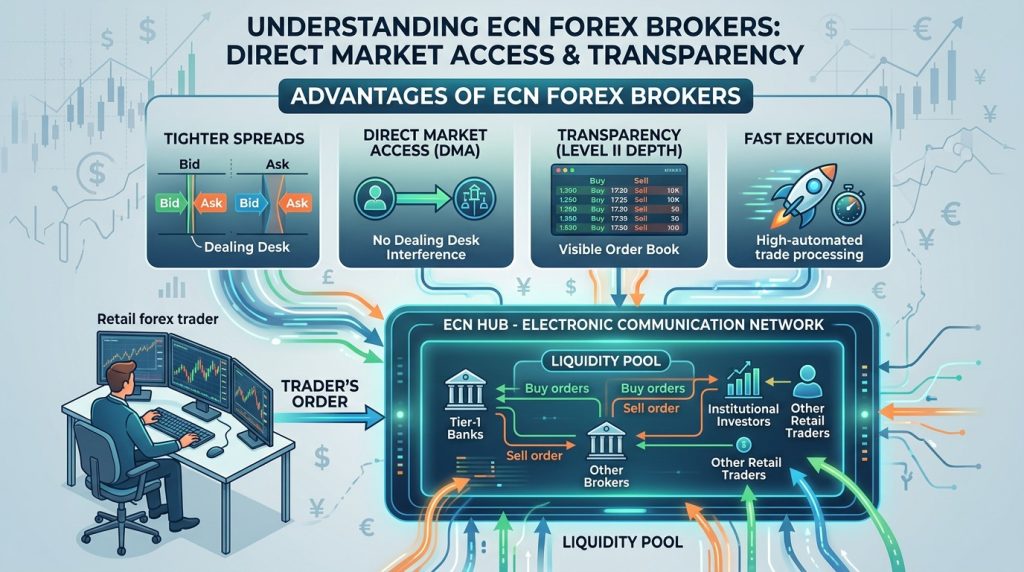

At its core, an ECN is simply a matching engine governed by a set of rules. Traders and institutions connect to the network—often through APIs or dedicated connections—and send in bids, offers, and orders.

For each instrument, the system maintains an order book. This book lists buy and sell limit orders at different prices and sizes, organised by price first and then by the time the order arrived. When compatible orders meet, the engine matches them and the trade is executed.

When a new aggressive order hits the system, the engine immediately starts matching it with existing orders on the opposite side of the book. It begins with the best available price and works its way through the order levels until the order is fully filled or there’s no liquidity left.

Each match becomes a trade. The system records the execution, updates positions and credit limits, and reshapes the order book as filled orders disappear or shrink in size.

In foreign exchange, ECNs usually host quotes from banks, non-bank market makers and larger trading firms. Some also allow certain clients to post their own firm prices, turning them into liquidity providers as well as takers. In equities, ECNs act like alternative trading systems, providing extra venues alongside primary exchanges.

The engine does not care who you are in any emotional sense. It applies the same rules to every order that meets its technical and credit requirements. That mechanical fairness is a large part of ECN appeal, even if the outcomes you actually get still depend on who else is in the book and how they behave.

Price formation and depth of book

Prices on an ECN are a direct result of what its participants are prepared to quote. The best bid is simply the highest price at which someone is willing to buy at that moment. The best ask is the lowest price at which someone will sell. The spread between them can be very small on liquid pairs and actively traded stocks when several firms compete for flow.

Depth matters as much as the top line. A tight spread with almost no size at the inside levels is not very helpful if you want to trade more than a token amount. A healthy ECN book shows layers of bids and offers at successive prices, each with meaningful volume. For large players, that depth is as important as the headline spread.

Retail clients using an ECN broker often see only the best prices, sometimes plus a simple depth ladder. Institutional users usually see full depth per venue, and their smart order routers decide where to send flow based on that picture.

This price formation process is why ECN quotes can look sharper than typical retail dealing desk quotes in quiet times and more ragged in stress. When the banks and dealers feeding the network pull back or widen spreads, the ECN reflects that instantly. There is no smoothing committee. If nobody is keen to show tight prices around a data release, the book shows that gap without apology.

ECN brokers versus classic market makers

Principal dealing and internalisation

A classic retail market maker takes a different route. The broker receives reference feeds from banks and other sources, runs them through a pricing engine and publishes its own bid and ask for each instrument. That engine can add mark-ups, apply filters, smooth out spikes, and even skew quotes a little when client flow becomes very one-sided.

When you trade on that quote, you usually face the broker as principal. If you buy one lot of EURUSD, the broker is short one lot to you. It can then decide whether to hedge that risk externally or keep it in house. If many clients buy, the broker’s book becomes short and its risk managers may choose to offset some of that with banks or ECNs. If client flow is roughly balanced, the desk may sit on it and collect spread plus the net outcome of that internal client game.

This is called internalisation. Client orders are matched against each other or against the house; only net residual goes out. It can be efficient and cheap to run. It also means your broker has a direct financial interest in how its book performs against clients.

An ECN broker, at least in theory, does less of that. It passes orders into a shared network rather than keeping them. That does not guarantee purity – brokers can still aggregate, split and sometimes internalise when they choose – but the core model is different. The venue where your order is matched is not owned or controlled by the broker itself.

How conflicts of interest change

Because a market maker can profit from clients who lose in a smooth, predictable way, the conflict of interest is baked in. Your trades are line items on the firm’s PnL. That does not automatically mean manipulation, but it shapes incentives. A broker in that position must work extra hard, and be watched extra closely, to avoid leaning on tricks that tilt the field: slow quotes for sharp traders, heavy slippage in one direction, or sudden spread blowouts around obvious stop zones.

In an ECN model, the broker’s income is more straightforward. It charges commission on each side of each trade, plus maybe a small spread mark-up, and pays the ECN and liquidity providers their share. The firm wants stable volume and decent relationships with its LPs. It does not need your trading to lose money; it needs you to stick around and keep trading.

Conflicts do not vanish completely. A broker may have better commercial terms with one liquidity provider than another and route more flow that way even when another venue shows a slightly better tick. It may offer re-quotes or reject orders when there is a sudden gap in its LP feeds. But the raw “we win when you lose” link is less intense.

For a trader deciding between broker types, that shift in conflict level is one of the main arguments for choosing a genuine ECN or at least an honest pass-through model instead of a pure dealing desk.

ECN brokers versus STP and “no dealing desk” models

Order routing and aggregation

Straight-through processing brokers sit between full ECN access and classic market making. They take quotes from several banks and dealers, aggregate them into a combined feed and route client orders to the provider quoting the best price at that moment, sometimes splitting orders across several.

From the client side, spreads look variable and close to interbank conditions. Commission may be charged per lot, or the broker may add a small mark-up in the spread. The firm claims not to run a dealing desk that takes the opposite side of client trades as a steady business.

The key difference is where matching occurs. In an ECN, you and other participants all send orders into the same shared book. Matching happens on that venue. In a pure STP model, the broker is more like a router. It sends your order out to one of several external liquidity providers with which it has bilateral relationships. You do not see or touch the central books directly.

Many retail “ECN accounts” are built on top of this plumbing. The broker connects to true ECNs and bank platforms, uses those as liquidity sources, and presents a combined feed to clients. Marketing uses the ECN label because the pricing comes from those venues, even if individual retail tickets do not rest as named orders inside the ECN itself.

Hybrid books and what really happens to flow

In practice, most retail brokers run hybrid books. They route some flow straight out (often called A-book) and keep some in-house (B-book). Small, noisy accounts that follow the usual losing pattern are cheap to internalise. Very sharp or large accounts are passed out to banks and ECNs more often.

That means a single client base at one firm can be split across handling models. Two traders on “ECN accounts” may see slightly different behaviour if their flow is classified differently. One might be hedged outside consistently; the other might be filled from an internal pool most of the time and only occasionally hedged.

The hybrid approach is not evil in itself. It is a sensible risk and cost management trick. The problem is opacity. Many brokers advertise “STP” or “ECN” without explaining that much flow still hits an internal book at some point. For a client, the only way to judge behaviour is to watch fills, slippage and spreads during quiet times and stress, not to rely on marketing tags.

So in the hierarchy you can think of it like this. Pure dealing desk: most flow stays internal. STP: more flow is hedged with outside LPs but matching is still bilateral. ECN: matching is on a shared venue where many participants meet. Retail “ECN brokers” sit somewhere between STP routing and true venue membership, depending on their size and relationships.

ECN, DMA and prime-of-prime access

Institutional ECN use

On the institutional side, ECNs and similar venues are routine. Banks, hedge funds and prop firms hold prime brokerage lines with large banks. Those lines let them face ECNs directly as named participants, with credit limits and margin supervised by their primes.

These players subscribe to several ECNs and single-dealer platforms, each with its own characteristics. They run smart order routers that decide, order by order, where to send flow: which ECN, which bank stream, which dark pool. They look at depth, fill ratios, historical slippage and information leakage before allocating flow.

For them, ECN access is not a badge to put on a website. It is the core of how they move risk. They pay with collateral, legal agreements, connectivity spend and sometimes very tight operational constraints in return for tighter spreads and better matching quality.

How retail actually taps that plumbing

Retail traders do not sit directly on that interbank layer. They do not have credit with banks or ECNs. Instead, ECN brokers and prime-of-prime firms sit between retail and the institutional pool.

A prime-of-prime aggregates liquidity from several ECNs and bank streams, then offers it on to smaller brokers. The retail broker in turn aggregates quotes from one or more primes and maybe some direct LPs, wraps a spread and commissions around them, and shows that to clients.

When you place a trade on a decent ECN account, the broker may send your order out as part of a bundled ticket into an ECN, hedge it as part of its net position at a prime, or internalise it briefly and only adjust the hedge book once net exposure has moved. Detail varies, but the pricing you see should track the institutional pool closely, and your fill should reflect what is actually tradeable, not a fictional internal price.

That is the real value of an ECN broker for a retail trader. You piggy-back on the same quotes and books that serious players use, without negotiating credit lines yourself. You still depend on the broker’s honesty and competence, but you are not sealed inside a closed pricing system.

Costs, fills and behaviour that traders will notice

Spreads, commission and slippage

The first thing most traders notice on an ECN account is spread behaviour. On liquid forex pairs, during active hours, raw spreads can be extremely tight. On some ticks the best bid and ask may be separated by a fraction of a pip. On a market maker account you would normally see something wider and smoother, because the broker has built its costs and risk premium into that spread.

ECN brokers make that difference up with commission. You pay a fixed fee per million of notional traded or per lot, on both open and close. To judge cost fairly you have to combine spread and commission, not look at either in isolation. For scalpers, that total per round-trip is critical. For longer-term traders, the difference between account types matters less but still adds up.

Slippage behaves differently too. On a healthy ECN feed, you sometimes get positive slippage when the book improves between the moment you click and the moment you are filled. You sometimes get negative slippage when it worsens. Over a decent sample, the distribution should be roughly balanced if routing is fair.

On a weak dealing desk, slippage can be more one-sided. Fills that benefit the broker appear more frequently than those that benefit the client. Close trades around news tend to resolve in the house’s favour. That is not inherent to dealing desks, but it is more common there because slippage rules sit entirely under the broker’s control.

An ECN broker that never shows positive slippage and always seems to slip in one direction is telling you something about how it handles flow, regardless of what it calls the account.

News events, thin markets and outages

ECN conditions during stress can surprise traders who are used to smoothed retail feeds. Around major data releases, spreads can widen sharply as banks pull quotes or reduce size. Depth can vanish for a few ticks. Market orders go through but at prices that reflect that temporary vacuum. Limit orders may be skipped if price gaps through them.

It can feel rough to be slipped heavily on a stop in that environment, but that is what happens in the underlying market too. A market maker may choose to soften that with artificial pricing or by filling stops at better levels than it could hedge at, but that is essentially a subsidy. ECN plumbing rarely gives you that.

Thin market behaviour is similar. During holidays or quiet sessions, spreads on an ECN feed will often show that quiet directly. If you insist on trading size during those hours, you pay for it in worse prices. On a fixed-spread retail account, you might see apparently normal spreads but then run into re-quotes and slippage when you actually hit the button.

Outages and disconnects are still a risk. An ECN broker is only as good as its tech stack and its providers. If the ECN itself goes down, or a prime has issues, your platform can freeze even though your internet is fine. Serious brokers publish incident reports and upgrade infrastructure after ugly episodes; weaker ones shrug and move on.

From a trader’s point of view, the main tell is transparency. A broker that openly documents spread behaviour, downtime and average fill stats is usually more trustworthy than one that stays quiet and hides behind vague “market conditions” statements every time something odd happens.

Who ECN brokers are best suited for (and who they are not)

Short-term active traders

Short-term traders who rely on narrow statistical edges naturally gravitate to ECN or at least clean STP models. If your average target is five pips and you take dozens of trades per week, every half-pip of cost and every millisecond of delay shows up in the stats. A market maker with inconsistent execution can wreck a method that would survive fine in a more transparent environment.

An ECN broker supplies variable, market-driven spreads, visible commission and more honest slippage. That does not make life easy, but it makes the bar clear. You either beat that stack of costs and noise or you do not. There is less mystery about where your edge went.

Algorithmic traders and those who use limit orders to provide liquidity also benefit from closer contact with the book. Being able to rest orders inside the spread and sometimes capture the bid-ask rather than always paying it can tilt the economics slightly in your favour, as long as you understand queueing and partial fills.

That said, running code on a retail ECN broker is not the same as sitting inside an HFT shop co-located at an exchange. You still contend with retail platform overhead and shared lines. The goal is simply to get close enough to real conditions that your short-term edge is about market behaviour, not broker quirks.

Swing traders and longer-term investors

Swing traders and position traders have more freedom. When your average stop is, say, fifty pips and your target is two hundred, the difference between a one-pip and a two-pip spread matters less than how honest the broker is on swaps, margin and stability.

For these traders, the choice between a decent ECN broker and a well regulated market maker is less dramatic. Both can work if costs are fair and conduct is sound. Some swing traders still prefer ECN on principle, to avoid any hint that their profits are someone else’s problem. Others are happy at brokers that offer good tools, clear reporting and a broad product set, even if execution is technically dealing-desk based.

Investors who mainly hold cash equities, funds or bonds rarely need ECN style access at all, unless they trade size or complex orders. Their broker selection revolves around custody safety, tax reporting, corporate action handling and so on, not microstructure in FX or index CFDs.

The traders for whom ECN really matters are the ones who live and die by execution. For everyone else, an ECN broker is a nice to have if price and regulation line up, not an automatic must.

One rule works almost everywhere: if a broker loudly claims to be an ECN but can’t clearly explain who its liquidity providers are, how it actually makes money, or what happens during volatile markets, the label doesn’t mean much.

The marketing tag alone isn’t proof of anything. You still need to check the firm’s regulation, read the terms carefully, and pay attention to how your trades are actually filled once real money is involved.

This article was last updated on: March 5, 2026