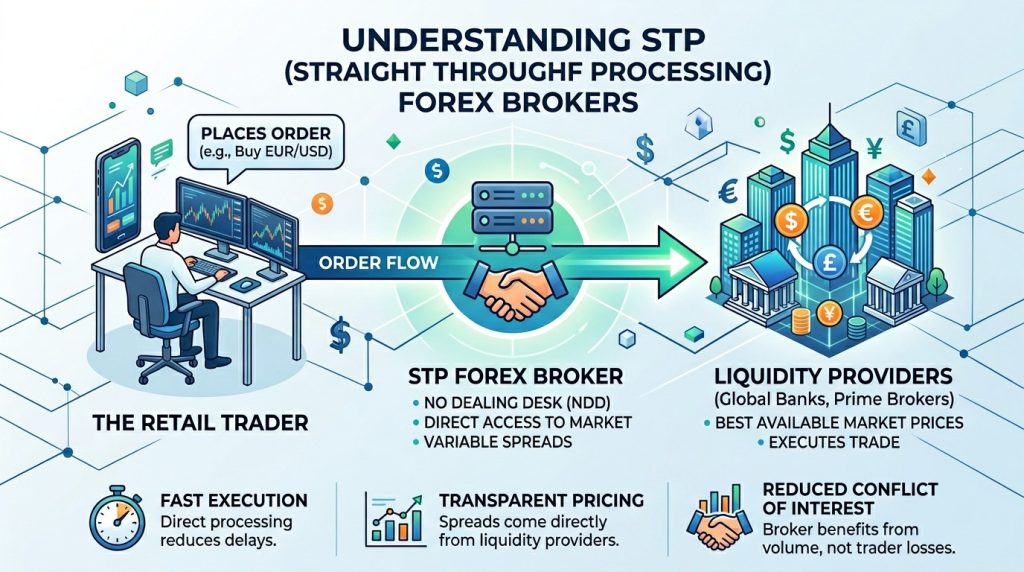

STP stands for straight through processing. In trading slang an STP broker is one that routes client orders out to external liquidity providers without manual dealing desk intervention on each ticket. Instead of a dealer sitting there “making a price”, the plumbing is automated. Quotes arrive from banks and other providers, a pricing engine builds a composite feed, and your trades are hedged outside the firm according to a set of routing rules.

The label took hold in retail forex and CFD markets as a reaction to classic dealing desks. Many traders started to question why their broker was both the platform and the house on the other side of their trades. STP sounded cleaner: the broker presents outside prices, passes your orders straight through, earns from spread mark-ups or commission, and does not sit there hoping you blow up.

Reality is more mixed than the slogans, but the core idea still matters. A genuine STP broker is closer to a router than to a casino. It tries to line up buy and sell interest on client accounts with bid and offer prices from banks, non-bank dealers and sometimes larger brokers. Instead of warehousing most risk against you, it sells that risk on and keeps a stable slice of the flow economics for itself.

To understand what that means for you as a trader, you need to see how STP routing actually works and how it compares, in practice, with both classic market makers and brokers that plug directly into ECNs.

This article will focus on STP forex brokers. If you’re a broker to open an account with then I recommend you go to Forex Brokers Online. Forexbrokersonline.com can help you find a forex broker that suits your needs.

How STP routing actually works

Price feeds, aggregation and the client quote

An STP broker usually connects to several liquidity providers. Those might be large banks, non-bank market makers, prime-of-prime firms or even ECN hubs. Each sends a stream of two-way quotes for each instrument. At any given moment the broker might see three, eight or more different bids and offers for EURUSD, for example, each with its own size and timestamp.

A pricing engine sits on top of these feeds. For each pair it picks the highest bid and the lowest offer across all providers and uses them to build a composite price. It can also look deeper into the book, keeping track of how much size is available one or two levels away from the best prices. On top of that the broker may add a tiny mark-up or mark-down to create its own quoted spread.

What you see in your terminal is this aggregated quote rather than a raw bank stream. If the broker chooses to keep mark-ups small and spreads mostly variable, your chart and bid-ask will track interbank conditions fairly closely. In quiet sessions spreads will tighten. Around events and in thin trading spreads will widen and may move around a lot.

This is one of the main practical differences from a classic retail market maker. On fixed-spread dealing desks the feed is often smoothed and clipped. Underlying interbank spreads might blow out, but the platform will still show the advertised fixed spread, at least until the firm pulls liquidity or switches to wider “emergency” pricing.

Order flow, hedging and where the risk ends up

When you press buy or sell, the order hits the broker’s server. The routing system checks where that order can be filled at the best price for the stated size. If one liquidity provider is quoting the inside bid or ask and has enough size to fill you, the system will send a hedge order there. If no single provider can take the whole lot at the inside price, the system can split the hedge across several providers at slightly different levels.

Some STP brokers hedge every ticket immediately, one for one. If you buy one lot of EURUSD, they sell one lot to a bank or prime at the same time. On the broker’s book you are not their market risk, you are a line of client risk with an offsetting hedge on the other side.

Others work at net level. They may let some client buys and sells offset each other internally, then only hedge the residual net position with providers. If a pool of clients ends up net long, the broker’s dealers will sell that net amount to their LPs. As long as this netting process is rule based and the hedge side is real, the setup still counts as STP. The broker is using internal matching to save on tickets, not to run a speculative book against its clients.

In either variation, revenue comes from spreads and explicit commission on the client side minus costs and fees paid to LPs on the hedge side. The broker wants steady, predictable flow and low rejection rates with its providers, not wild wins and losses on a B-book.

STP brokers compared with classic market makers

Who stands on the other side of your trade

In the classic retail model, the broker quotes a price, you trade on that quote, and they stand on the other side as principal. If you buy, they are short to you. They can then choose to keep that risk or lay it off. Many dealing desks split their book into an A-book (hedged trades) and a B-book (internalised trades). New, small or consistently losing clients are often left on the B-book. Their trades never reach outside liquidity; the firm simply accepts that on average those accounts will lose.

That approach means that a big part of the broker’s income is the net loss of B-book clients. Spread and swaps matter as well, but the house position against those accounts is a profit centre.

An STP broker, at least as a base design, moves away from that. When you buy, the other side of your trade is supplied by some mix of banks, non-bank dealers and other outside LPs. The broker’s risk team still monitors net exposures, but its default assumption is that it will not carry large, directional positions versus its own client base. It prefers to pass that risk out and collect a fairly stable revenue share on the flow.

From your view that changes who you are playing against. In a dealing desk your gains are partly the broker’s loss, and vice versa. In an STP setup your gains are paid by whoever is on the other side of your trade through the LP network. The broker sits in the middle as a toll collector instead of as your opponent.

How conflicts of interest change in practice

Conflicts never disappear completely, but they do change shape. A dealer that profits directly when B-book clients lose has a strong temptation to lean on grey-area practices: asymmetric slippage, slow execution for sharp accounts, sudden spread shifts around common stop levels, and so on. A well run, tightly regulated dealing desk can resist that, but the raw incentive is still sitting there.

On an STP model the broker’s income is not as directly tied to client loss. It earns when you trade, not especially when you blow up. An active client who trades for years and makes money is at least as attractive as a short-lived loser, maybe more so. The firm wants to keep such clients and keep LPs happy by sending them flow that behaves well.

There are still softer conflicts. A broker might receive better commercial terms from one liquidity provider than another and route more volume there even when another venue shows slightly better tick prices. It might widen spreads on certain pairs to protect its own economics. It might choose to A-book or B-book some flows for operational reasons. But the hard “we win when you lose” linkage is weaker.

For a trader, that shift matters. You still need to watch execution and fee schedules, but you are not automatically sitting at a table where the house directly profits from your ruin.

STP brokers compared with ECN brokers

Matching engine versus smart routing

An ECN is a central matching venue. Participants place bids and offers; the engine matches orders according to price and time. When you trade through a true ECN broker, your orders are meant to rest, at least in aggregate, in that shared order book. Fills come from other participants on the ECN.

An STP broker uses a different pattern. It does not usually expose your orders as resting quotes on a venue. Instead it listens to the quotes that banks and ECNs send, constructs its own feed, and uses smart routing rules to send hedge orders back out to those same sources. Matching happens either inside those external venues or bilaterally with LPs, not in an order book that your own orders sit in under your name.

From a retail seat the difference is partly about visibility. ECN accounts at some brokers offer depth of market views, so you can see several levels of bids and offers. You might also receive tiny rebates when you add liquidity with limit orders at attractive prices. STP accounts often show only the top of book and treat all client orders as liquidity-takers internally.

The machinery is similar on the back end. Both models connect to LPs, ECNs and primes. Both have to manage routing and credit. The question is whether you, as a client, are a named participant inside the ECN’s order book or a consumer of a composite stream that someone else builds for you.

Cost structure, minimum size and depth

ECN pricing is usually “raw spread plus commission”. On highly liquid pairs raw spreads can be extremely narrow, even close to zero at times. Commission per million traded or per lot becomes the main explicit cost. You get close to whatever the ECN is showing.

STP feeds are often priced the same way from a client point of view. The broker shows tight variable spreads and adds a ticket fee. Under the hood it pays a slightly smaller spread and fee to its LPs and keeps a mark-up. In other words, your “ECN account” at a retail broker is often riding on top of STP routing to one or more real ECNs.

Minimum size is where a clear gap appears. True ECN venues like to deal in reasonable clips. Micro-lot trading is not their game. Retail brokers know that many clients want to trade very small sizes, so on both STP and ECN-branded accounts they accept tiny orders, group them, and hedge only once size is economic. That means your 0.01 lot EURUSD trade does not hit an ECN as a discrete order. It is part of a batch that the broker manages.

Depth matters more for larger traders. If you run size, knowing that several million sits one or two pips away from the best price is vital. Direct ECN access gives a clean view of that depth. STP brokers may only show the inside price while still using LP depth for routing. Retail traders with small accounts rarely hit those size issues.

For most private traders the practical distinction between a good ECN broker and a good STP broker is not the label but how honest the pricing and routing are, how tight spreads and commissions are in practice, and how the firm behaves under strain.

Hybrid books, A-book and B-book reality behind “STP only”

Why almost nobody runs a pure model

Running a pure A-book, where every client ticket is hedged externally straight away, sounds clean. In reality it can be inefficient. Very small trades, random in direction, just add ticket costs and LP charges if hedged one for one. They do not change net risk much. It makes sense for a broker to net such flow internally and only send the residual to LPs once it reaches a sensible size.

That is where hybrid books come from. Instead of two separate firms, you get one broker with internal books and external routing. Desks inside the firm decide which flows can safely be internalised for a time and which must go out immediately. Risk managers set limits and monitors to avoid large unhedged exposures.

On paper many brokers still call this “STP”, because they do use straight through routing for a fair chunk of client volume. The marketing material tends not to mention that there is also a B-book running for a subset of the flow, especially for small, new, or obviously random accounts.

Pure STP and pure ECN exist more on institutional desks and bank-to-bank platforms where ticket sizes are large and flows are more predictable. Retail access almost always passes through at least one hybrid layer, even when the surface label is neat.

What this means for fills, slippage and “sharp” clients

For an individual trader, the hybrid reality shows up in a few places.

If your account is small and you trade in tiny clips with no clear edge, a broker can internalise that comfortably. You may experience very smooth fills in normal times and think of the firm as very “liquid”. Behind the scenes, risk managers see that your flow nets out with that of other clients and barely touches the LP pool.

If you start to trade larger, win more often, or run a recognisable strategy that stresses the broker’s quotes, your orders may quietly move to A-book. That is usually good for you. Your trades are hedged outside, and the broker treats you more like an institutional client from a risk view. On the other hand, you may start to notice “real market” behaviour more clearly. Spreads widen more around news, slippage becomes more symmetric and less smoothed.

Slippage patterns can be a useful clue. When internalisation is heavy, brokers can decide how to share price improvement. They could keep most favourable ticks for themselves and pass worse ones on to clients, or they could split them fairly. Over a large sample of trades, a strongly skewed slippage record is a warning sign, whatever the brochure says.

For very sharp traders running latency-sensitive methods, some brokers will resist keeping flow internal at all and will A-book them aggressively or even ask them to leave if the economics do not work. That is less about STP versus ECN and more about whether the broker’s LPs are happy to face that flow.

The takeaway is that you can not treat “STP” as a magic shield. You still need to monitor your own fills, check how the firm behaved during events in the past, and read complaints with a critical eye. The plumbing can be well designed and still be used in ways that favour the broker more than you.

What matters most in an STP broker for active traders

Spreads, commission and swaps

From a working trader’s point of view, the mechanics of STP matter because they shape three numbers: the spread you pay, the commission per trade, and the overnight swaps or funding charges.

Tight, variable spreads that track interbank levels keep entry and exit costs low. If a broker claims to be STP yet shows wide spreads in quiet markets, something else is going on. Commission should be clear, per lot or per million, not buried in vague phrases. When comparing brokers, it makes sense to calculate all-in cost per round trip on the pairs and sizes you actually trade.

Swaps are easy to overlook. Many STP brokers quote swaps directly based on LP funding plus a mark-up. If you hold trades overnight as part of your style, those charges add up. Carry-heavy pairs can grind a small edge into nothing if the broker’s mark-up is large. On index and commodity CFDs, daily funding can vary a lot between firms using the same STP pitch.

Transparency helps here. Some brokers publish live swap tables, explain how they set them and update them regularly. Others barely mention swaps in marketing, then silently widen them. For a trader trying to swing positions over days, the second group is an expensive habit.

Execution quality, rejects and behaviour in stress

Execution quality is the practical test of an STP setup. You want orders filled at or near the quoted price most of the time, with occasional positive and negative slippage that sits in a reasonable band. You want very few unjustified rejections. When rejects do happen, you want clear reasons like “price moved beyond your tolerance” rather than generic errors.

News events and flash moves are where STP routing really shows itself. During those patches spreads widen and some LPs may step back. A decent broker will still route orders based on real prices and will not try to pretend that liquidity exists where it does not. Stops may slip; that is part of trading live prices. What you do not want is a platform that freezes, re-quotes after the fact, or retroactively cancels fills.

Past behaviour is a better guide than any brochure. If a broker stayed online and processed trades during major incidents without retroactive changes, that earns trust. If it has a track record of “trade adjustments” after volatile days, it does not matter how big its STP logo is.

For an active trader choosing an STP broker, boring traits count most. Honest spreads, clear fees, stable platforms and grown-up communication when something breaks matter far more than flashy promos or heroic language on the front page.

Which traders fit STP brokers best

Short term methods

Short term traders who care about execution but do not need full ECN depth often sit right in the target zone for STP brokers. If you work off the one-minute to one-hour chart, take several trades per day or week, and lean on tight stops, consistent pricing and decent fills help a lot.

A well run STP broker gives you most of the good parts of ECN access — realistic spreads, fair slippage, variable pricing that reflects real conditions — without forcing you into institutional-size tickets or heavy data costs. You can trade micro lots while still seeing a feed that largely tracks what banks are quoting.

Scalpers at the extreme end, who lean on tiny statistical edges and latency tricks, may still want direct ECN membership or relationships through prime-of-prime firms. But for the vast majority of active retail traders, honest STP routing is close enough to the underlying market that the bottleneck is their method, not the pipe.

Swing and longer hold methods

Swing traders and longer hold traders can work with either STP or market maker brokers, as long as the firm behaves sensibly and costs are acceptable. For them, the main upside of an STP model is peace of mind about conflicts. It is easier to focus on trade logic when you are not constantly wondering whether someone at a dealing desk is cheering for your stop to be hit.

If you hold positions for several days to weeks, spreads on entry and exit matter less than swaps, margin policy and stability. Many STP brokers handle swaps reasonably and follow the same margin standards set by regulators in larger regions. That gives you a predictable framework for planning your risk per trade and portfolio-level exposure.

For investors who mainly deal in cash equities, funds and long-term holdings, the STP tag is mostly irrelevant. Their brokers might still use STP for internal FX or derivative hedging, but as clients they interact with an order system built around exchanges and central clearing, not around bilateral LP streams.

In short, STP brokers sit in the middle of the brokerage map. They are not magic, and they are not all honest. But when the plumbing really does push most of your flow through outside liquidity instead of sitting on the other side of your book, the structural incentives line up closer with what an active trader actually needs: stable, transparent access to a market that is already hard enough without a dealing desk leaning on the scales.

This article was last updated on: March 5, 2026